Page 62 - MC14326 all pages

P. 62

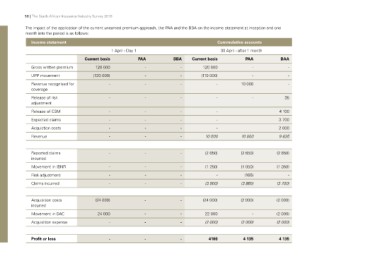

58 | The South African Insurance Industry Survey 2016

The impact of the application of the current unearned premium approach, the PAA and the BBA on the income statement at inception and one

month into the period is as follows:

Income statement Cummulative accounts

Gross written premium 1 April - Day 1 30 April - after 1 month

UPP movement

Revenue recognised for Current basis PAA BBA Current basis PAA BAA

coverage - -

Release of risk 120 000 - - 120 000 - -

adjustment - -

Release of CSM (120 000) - (110 000) -

Expected claims 35

Acquistion costs -- - 10 000

Revenue 4 100

-- --- 3 700

2 000

-- -- 9 835

-- --

-- --

-- - 10 000 10 000

Reported claims - - - (2 650) (2 650) (2 650)

incurred

- - - (1 250) (1 050) (1 050)

Movement in IBNR - - - - (165) -

- - - (3 900) (3 865) (3 700)

Risk adjustment

Claims incurred

Acquisition costs (24 000) - - (24 000) (2 000) (2 000)

incurred

Movement in DAC 24 000 - - 22 000 - (2 000)

Acquisition expense - - - (2 000) (2 000) (2 000)

Profit or loss - - - 4100 4 135 4 135